Insurance these days is a divisive topic in the U.S. and if you look at the numbers for health insurance costs over the last decade or so, it’s not hard to see why. Just take a look at these charts from the Kaiser Family Foundation:

Cumulative Increases in Costs 1999-2012

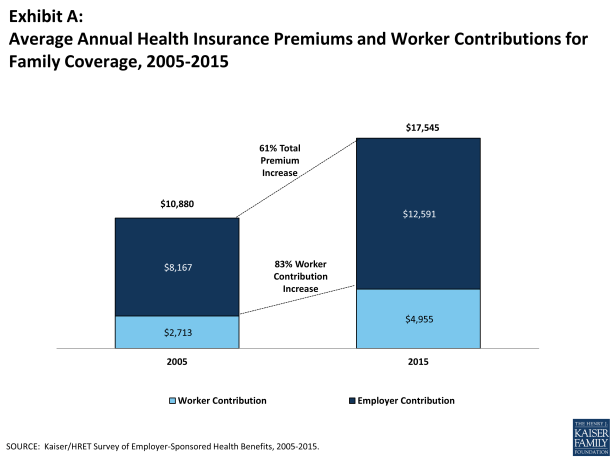

2005 vs. 2015 Cost Comparison

Unfortunately, even though we have insurance systems in desperate need of reform, insurance is still one of the best tools for building financial freedom and wealth. Here are a few questions to consider when thinking about how to pick the best products for you and your lifestyle.

Do I Need Insurance?

If I could say “yes,” end of story, and readers take it seriously, I would. But as it is, I know some may need convincing. The sad reality is close to what Tim Keller wrote in a recent book:

“No matter what precautions we take, no matter how well we have put together a good life, no matter how hard we have worked to be healthy, wealthy, comfortable with friends and family, and successful with our career — something will inevitably ruin it.”

No one likes to think about car accidents, house fires, theft, serious illness, unexpected deaths, or other misfortunes – especially when placed in the context of your immediate family or your possessions, but the sad truth is that these things are much more common than we like to think and our thinking about risk is (generally) unavoidably skewed. We almost always are wrong about the likelihood of something happening to us, so it’s worthwhile to be prepared.

What Kind of Insurance Do I Need?

This is not to say that you need to purchase insurance on every item you purchase – in fact, Dave Ramsey has some pretty good insight on why that kind of insurance is unnecessary. If you can’t afford to replace a product (for example, a cell phone or computer), that product is actually out of your price range (even if you think you can afford it).

The four types of insurance that I would recommend for most readers according to my own experience, my reading, and my insight into others’ experience are listed below:

Homeowners/Renters Insurance:

For renters, this is an especially easy proposition. You simply assess the worth of the items in your home and you will generally get a fairly low monthly quote. Make sure to consider all of your valuables, including jewelry, electronics, etc. Sometimes you can bundle this type of insurance with your auto insurance for a better rate as well.

Sometimes these insurance plans will cover damage occurring to someone else’s property if they are in your home or on your land – this is worth checking out when you are shopping around. Additionally, some policies extend to your valuables even when you are traveling with them – again, it’s important to read the fine print to know exactly what is covered and what is not. You definitely don’t want to be left out in the cold if you have a flood, or some other disaster, but that isn’t covered in your policy.

Health Insurance:

No one ever wants to believe they will get more than your average cold or stomach bug, but unfortunately, we can find ourselves in a real pickle if we’re facing a more serious health challenge without the help of a personal insurance policy. I understand that this is particularly expensive in our nation at the moment and that there is a great need for reform; nonetheless, it is important to sit down with a disinterested party (that is, someone who cares about you and isn’t trying to make a sale) to figure out exactly what kind of coverage would be best for you with your age and risk factors taken into consideration. Even if you end up choosing a low premium, high deductible plan (that means you pay just a little each month, but if something were to happen you might still owe up to $7,000-$12,000 or more) it will still be a massive help and stress reliever if you end up with a condition that you can’t ignore, avoid, or control.

Auto Insurance:

While not all states require auto insurance (most notably New Hampshire and Virginia, which have other fees and requirements for drivers), the likelihood of having a major auto repair (or several) at some point while you own your vehicle is quite high. While the average cost of car repairs can vary widely by state, the national average puts costs between $300 and $3,400 depending on the type of service your care requires. Considering the fact that an accident generally results in repairs for two vehicles, rather than just your own, and that drivers have 3-4 significant accidents in the course of their “driving lifetime,” that makes reasonable insurance a good investment. Add to that the fact that your car insurance can cover things like towing costs and rental vehicles and you’ve got yourself not only financial savings, but time and stress savings as well.

Life Insurance:

If you don’t have a spouse or any dependents, this may be a non-issue for you, but otherwise, it is wise to look into life and potentially long-term disability insurance for the sake of those around you. While none of us want to imagine leaving our spouse or children with not only grief, but a litany of end-of-life costs, this can be the reality for many people who have not taken the time to think about this uncomfortable topic. Life insurance, in particular, is fodder for innumerable scams, so please do extensive research and talk to several knowledgeable people you trust before making any decisions, or any payments.

What Else Do I Need to Know About Insurance?

- Read all the fine print before signing anything and don’t be afraid to ask clarifying questions if there’s something you don’t understand. Better to look dumb at the insurance agent’s office than to feel dumb when you’re saddled with thousands of dollars in bills and don’t have any assistance from your insurance company.

- Shop around by looking at comparison quotes and doing your research. It’s always good to talk to someone else who has gone through a major difficulty (i.e. flood, fire, major illness, death of a loved one) to get their perspective on things they wished they had known or things that helped them immensely – just be delicate and compassionate if you broach the subject and make sure they are willing to share.

- Don’t sign anything until you know exactly what you’re getting. When we moved across the country last year, our auto insurance provider did not have a partner organization in our new region, meaning we had to find a new provider. Having known my old provider nearly my entire life (the couple that ran the franchise were old family friends), this was a major life change that I felt unprepared for. I did a lot of looking around, reading complicated policy briefs, and doing like-to-like comparisons. I quickly realized the policies that were “such a great deal” didn’t have nearly the coverage that our old policy had from the get-go, so I made sure we selected all the options we thought we would likely need, even though it meant we paid a little bit more per month than our old premium. Glad we did too, since we’ve needed towing and sundry services since the switch.

If you have any questions about insurance, Dave has some great insight on his website and radio show that can help point you in the right direction. Hopefully this post has encouraged you to cover all your bases in your journey to financial freedom!

Great post. It’s so important to read insurance information very closely to know exactly what to expect!

LikeLike

Thanks Brian! Yes, we almost learned this the hard way!

LikeLiked by 1 person